Co-buying property with friends

Learning to love The Process

[Note: I gave a webinar on this topic in July. You can find that recording here]

This is a long and detailed post for a very specific audience.

The audience is people who will soon go through the process of co-buying property as a group.

A more accurate description might actually be “a process” rather than “The Process.” There are a lot of ways to go about this. Here is simply one that we think works well for most people in most situations.

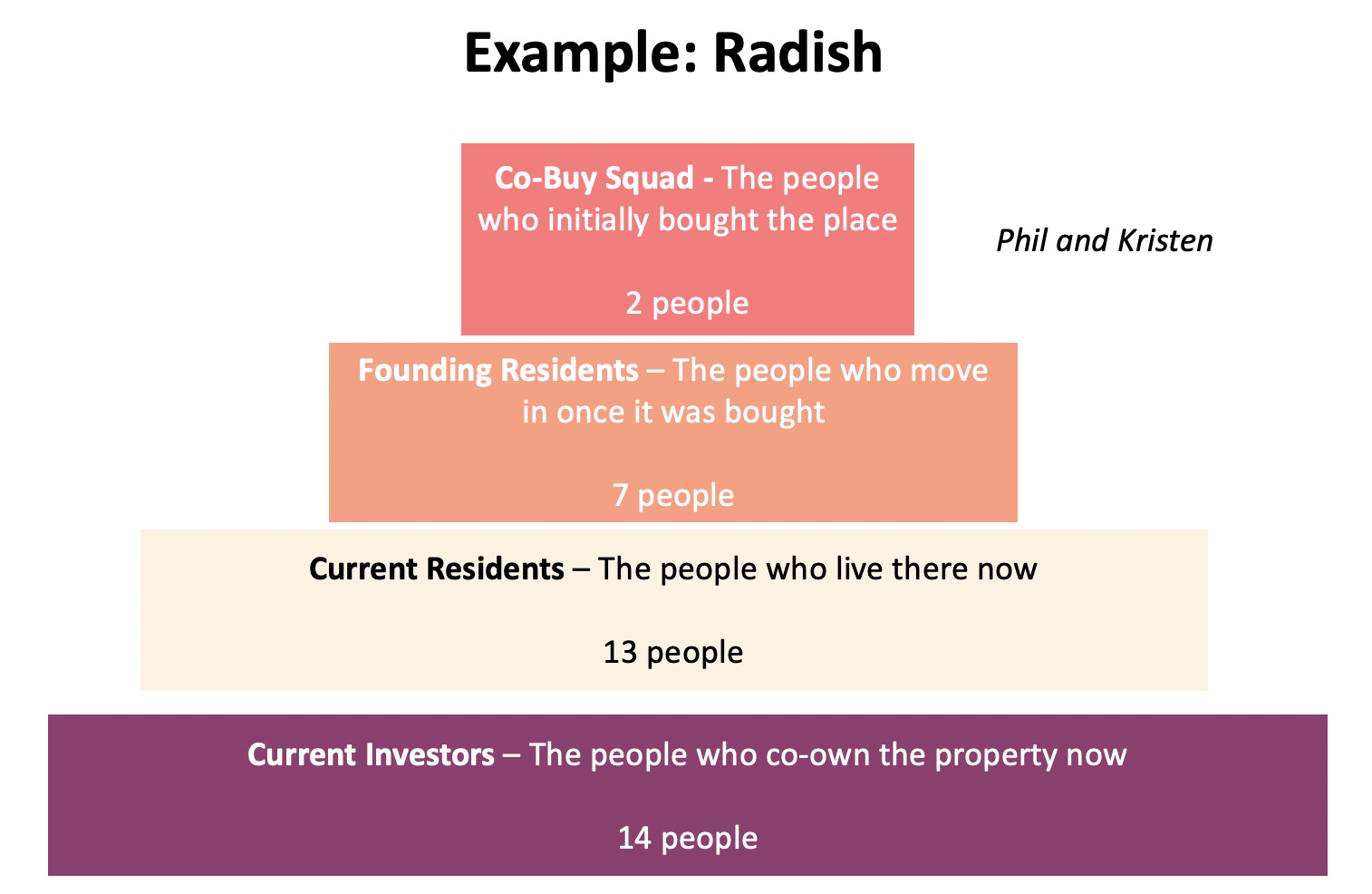

We’ll use Radish - our co-bought property in Oakland - as an illustrative example throughout this post.

Learning the love The Process

Lots of people say they want to write a book. Very few people actually do.

Co-buying property is similar. Many people idly wonder how great it would be to co-own property with their closest friends. Most of these people will end up living alone or with their nuclear families.

What anyone who actually writes a book will tell you is that the most important part is good process. It’s easy to write when the words are flowing. But you also need to have a process you can rely on when writing becomes a slog.

Co-buying property is similar. It can be a slog. There will be setbacks and obstacles. To get through the slog, you need to employ a good process and learn to love The Process.

Good Process = the possibility for community.

Bad Process = no chance.

What makes it hard? Simply put, the world of real estate is not designed to accommodate co-buying property.

Our financial system is designed for single or couple owners —> You’ll likely need to raise financing from multiple parties and structure it creatively

Existing building infrastructure is designed for single people and nuclear families —> You’ll likely need to renovate or build space to make it work for a larger group

Our zoning code has never heard of coliving —> You’ll likely need to apply for permits that are not easy to get if you need to build something

But the reward is there. And, weirdly enough, you’ll come to love The Process of getting there too.

Onward….

This post will cover four topics:

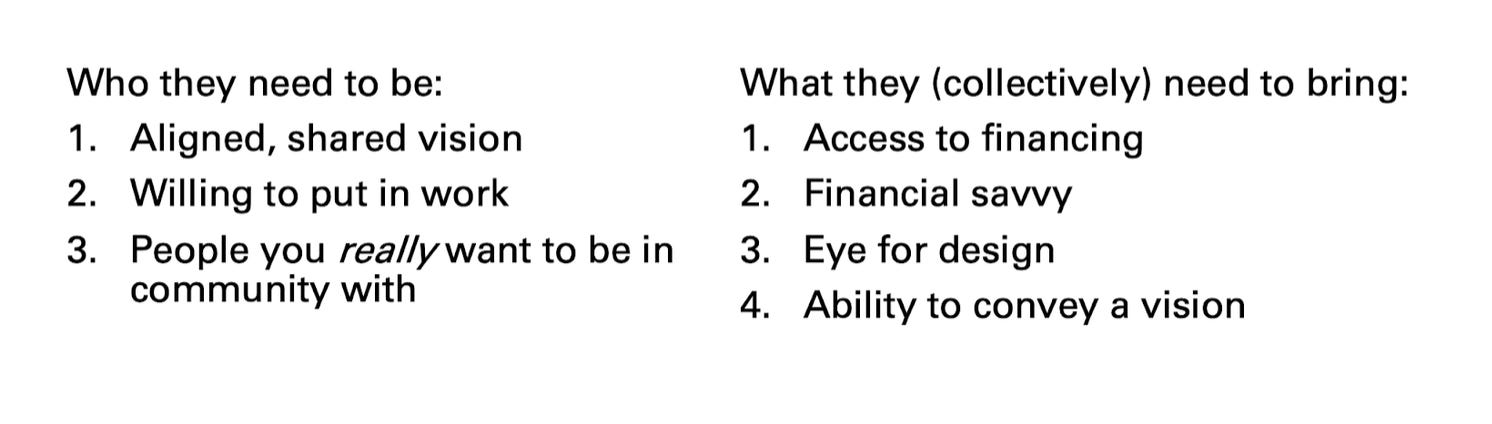

The Who: Pick Your Co-Buy Squad

The Who is the foundation. Be sure you are building your dream on a strong foundation. The Who in this case, is not every person who you might live with in the future. It’s just the people who are going to be involved in the initial purchase of the property.

Here is what the co-buy squad needs to bring to the table in order to be successful.

Common mistakes we see with The Who:

Fuzzy squad: Be sure you know who The Who is. It should be crystal clear to all participants who is part of the squad and who is not. It’s impossible to get alignment amongst a group that is fuzzily defined.

Dead weight participants: There is a real cost to gaining alignment and trying to triangulate people’s needs. Make sure you are working with people who are actually going to help make your dream a reality .. not just people who are willing to show up to a meeting or respond to a Facebook post. Less-committed people can participate later as residents or subsequent investors. You want a rock solid core in your co-buy squad.

Not having access to financing: All the enthusiasm in the world won’t help if you need a $400k downpayment and your Co-Buy squad doesn’t have it. You need people in your co-buy squad with financial resources or access to financial resources through friends or family.

The What: Define basic project requirements

aka distinguish “must haves” vs “nice to haves”

Here are the 4 basic factors we encourage people to define upfront when embarking on a co-buying project:

Geography

# of people who will live there

Must have features (short list!)

How fancy - We like to use the Yelp scale ($ through $$$$)

Example: How we defined “The What” at the Radish

Geography: <35 minute public transit commute to San Francisco (jobs)

# of people who will live there: 10-15

Must have features: Nice outdoor space, 3+ private units that could accommodate families

How fancy: $$

Common mistakes we see with The What:

Too broad on geography: The search for properties becomes never-ending if you don’t take a specific stand on where you want to live. And it becomes difficult to compare projects to one another.

Not having the awkward “how fancy” conversation: Misalignment here can tank a project.

Getting too specific on requirements: You’ll need flexibility to pull this off. Real estate constraints like availability and zoning will reduce the number of viable projects quickly. Don’t confuse “nice to have” with “must have.”

The How: Locate financing and define legal structure

This is the biggie. And depending on how things play out with the various steps, you may be forced to go back to “The Who” or “The What” if the financing is not there. We’ll break this up into 5 sub-steps.

Step 1: Estimate your total project cost (“TPC”)

TPC is the cost to purchase the property plus the cost of any critical renovations or building needed before people can move in.

If you are buying a house and moving right in, the TPC would just be the cost of the house. If you are buying an empty piece of land and then building 5 tiny homes on it, the TPC would be the cost of land plus the cost of the tiny homes.

The best way to do this is to estimate three factors:

Cost per square foot (sqft) for real estate in your area. Zillow has charts for this for each city. Oakland is $521 average so we said $500-600 (the Bay Area is heinously expensive).

Square feet needed per person: We thought 300-500 is the right range. RGB was about 300 sqft per person, which was dense but livable. 500 is roomier but still urban.

Number of people: How many people do you want to live on the property? We started with a target range of 1-15.

Multiplying these three factors at Radish gave us an estimated TPC of $1.5-$4.5m. We expected ourselves to likely be in the middle of this range so started preparing for a $2m - $3m project.

Step 2: Estimate down payment (aka cash needed)

Next step is to figure out what your downpayment might look like. This will be an important “uh, can we actually pull this off” moment. If you don’t think your co-buy squad has access to enough cash for the downpayment, you need to return to either “The Who” (get more people with more financial resources) or “The What” and downsize your project requirements.

Step 3: Decide what financial contributors get

Ok, so now you know your downpayment needs. And if you are buying a property for a big group, it’s likely to be a big scary number (we had a moment of hyperventilation when we first calculated this for the future Radish).

People are going to need to put in some serious cash. So you’ll need to quickly figure out what they get in return for doing so.

Here are what we see as the “Big 3 Questions”

Is there a financial return? How much?

This is an important fork in the road. You are likely in one of two places here. Either your residents are just going to buy their space and not pay rent (a la cohousing) or they are going to pay rent to whatever entity owns the space.

In the first scenario, the financial return is the same as it would be for anyone who buys a home to live in. The home might go up in value or down, but there’s no profit being created month to month from rent.

In the second scenario, there is the opportunity to create a monthly income. And that opportunity means that investors can get paid a regular financial return.

When thinking about the amount of return, it’s likely good to benchmark off of where people might be investing their money otherwise. The S&P 500 returns about 8% per year in the last 50 years. Bay Area real estate might return 4-6% each year in rental income (not including appreciation).How/when can I get my money back?

A few options:Dunno, your money is tied up for an unknown amount of time

We will sell the property in X years and you will get your money back then

New residents in the future will be required to put money into the project

We will refinance the project, which will produce extra cash (sometimes called a “takeout” or “cash-out refi”). You will get your money back then.

What investors will want to know is when any of these things might happen. You should have some idea of when the property might be sold or a solid story about how/when/why other people may come buy them out (and how the price would be determined).

Who makes the big money decisions?

Big money decisions include … when do we sell? …. do we do a major renovation? … do we refinance the property? … how much will rent be?

Financial contributors will want to know who is making those decisions and whether they have any input.

Common ways to handle this include 1) having financial contributors “vote” weighted by how much money they contributed 2) appointing a single “manager” to make decisions on behalf of the group 3) doing a combination of #1 and #2 where most day-to-day decisions are made by a manager but some big decisions (e.g. when do we sell?) are made by a vote of the financial contributors.

The below shows how we answered the Big 3 Questions when starting up the Radish.

A couple notes here:

We decided early on that residents will pay rent, which would provide a way to produce a regular profit for financial contributors. We wanted flexibility and inclusivity on who lived there (rather than requiring residents to “buy” their share of their living space). Rent is a good way to do this.

We decided early on that Radish was going to be a “now place” but not a “forever place.” It was going to be our ideal living situation for the next 5-10 years, but not until the end of time. This allowed us to tell financial contributors that we’d sell within 5-10 years so they can get their money back. Perpetual communities are, structurally, much more complicated.

We consider ourselves “stewards” of Radish - and made clear to financial contributors that they are essentially putting their trust in us and that their contribution would be passive from a decision-making perspective.

Step 4: Get soft commitments (awkward convo time!)

Now that you know the cash you’ll need and have answers to the Big 3 Questions, it’s time to go out into the world and have those awkward money conversations. It’s no longer hydroponics, tiny homes, and roses. Now it’s checking account balances and expected returns.

Go get soft commitments. Here is what a soft commitment sounds like:

“I will likely put in $100k if you buy a property within the next year along the lines of what you proposed”

A soft commitment should have 1) an amount of money 2) a timeframe 3) an acknowledgment of The What and the Big 3 Questions. A commitment that doesn’t include all of these is a fuzzy commitment and you need real commitments at this stage, not fuzzy commitments.

These are not the kinds of conversations we are used to having with friends. They are uncomfortable. Just channel your best Zach Galifianakis and learn to love them.

Step 5: Validate bank financing is available - *Do a dry run*

[Loans are a big topic. Here is a longer Supernuclear post on how to think about them.]

Okay, so you have soft commitments for cash. Great job!

Next step is to validate that a bank will lend you money. And make no assumptions here … banks are not into co-buying. You need to make this work for them.

They will finance single-family McMansions in the suburbs all day long. What you are doing will be less comfortable and familiar to them.

This is why we recommend testing financing before you make an offer. By the time you’ve made an offer, it may be too late to go back and forth with a bank. And it would really suck to lose your dream property because you didn’t do your homework.

First, figure out who is going to be on the loan

Is the entire co-buy squad going to be on the loan? Will one person shoulder the burden?

Note that banks typically will not allow more than 4 people to be on a loan. So don’t come to them with a dozen people. You likely want the minimum number of people who have the aggregate financial resource to qualify.

Next, find a “lookalike property”

Before you’ve found your dream property, pick a property which is close to your dream property but you don’t intend to actually buy. It should be roughly in the same price range and a similar type of property (e.g. empty land, apartment building).

This will become your test property for seeing if you can get a loan.

Tell a wee little lie…

Now you go to lenders and tell them (with a straight face) that you are most definitely interested in buying your lookalike property.

They will then take you through the underwriting process. They will assess your creditworthiness. They will assess whether they want to lend against that type of property. You will learn A LOT in this process.

At the end, you’ll either get a '“pass” or an indicative term sheet with interest rates and other terms. This is really helpful info and will prepare you for the real deal.

And you might not get any term sheets at all. If this is the case, you need to go back and either adjust your co-buy squad (to beef up the financial strength in the eyes of the bank) or adjust what kind of projects.

Some considerations on types of loans:

There are two main types of loans you’ll consider: A residential or a commercial loan.

Generally, if you can do a residential loan, you’ll want to do a residential loan. If you can’t, you’ll want to consider a commercial loan.

Residential loans are underwritten on the financial strength of the borrowers - essentially your credit score, income, and assets. The main thing they look at is whether your income is sufficient to cover the loan payments plus a margin.

Commercial loans are underwritten on both the financial strength of the borrowers and ALSO the income-producing potential of the property.

For a commercial loan you’ll need to put together a “pro forma” which is a financial model estimating what kind of income you could make off of the property. The bank will want to see that the income covers the loan payments plus a safety margin (see: Debt Service Coverage Ratio).

Note: Multi-unit residential loans may also require a pro forma to indicate what rents you may collect from the units you are not living in.

Strong advice: Talk to a bunch of banks

There are few things that can save you money more than shopping around for bank loans. There is wide variability here. And a few extra phone calls can save you $10k or even $100k over the course of a loan.

You’ll want to talk to different types of banks. There are big national banks whose names you hear whenever there’s a $1 trillion bailout. There are small regional banks whose branches you see in strip malls. There are purely online lenders like Quicken Loans. There are also “agency” lenders which do commercial loans on behalf of Fannie Mae and Freddie Mac. All of them might be the best lender for your specific situation.

Get a feel for all of them that are relevant.

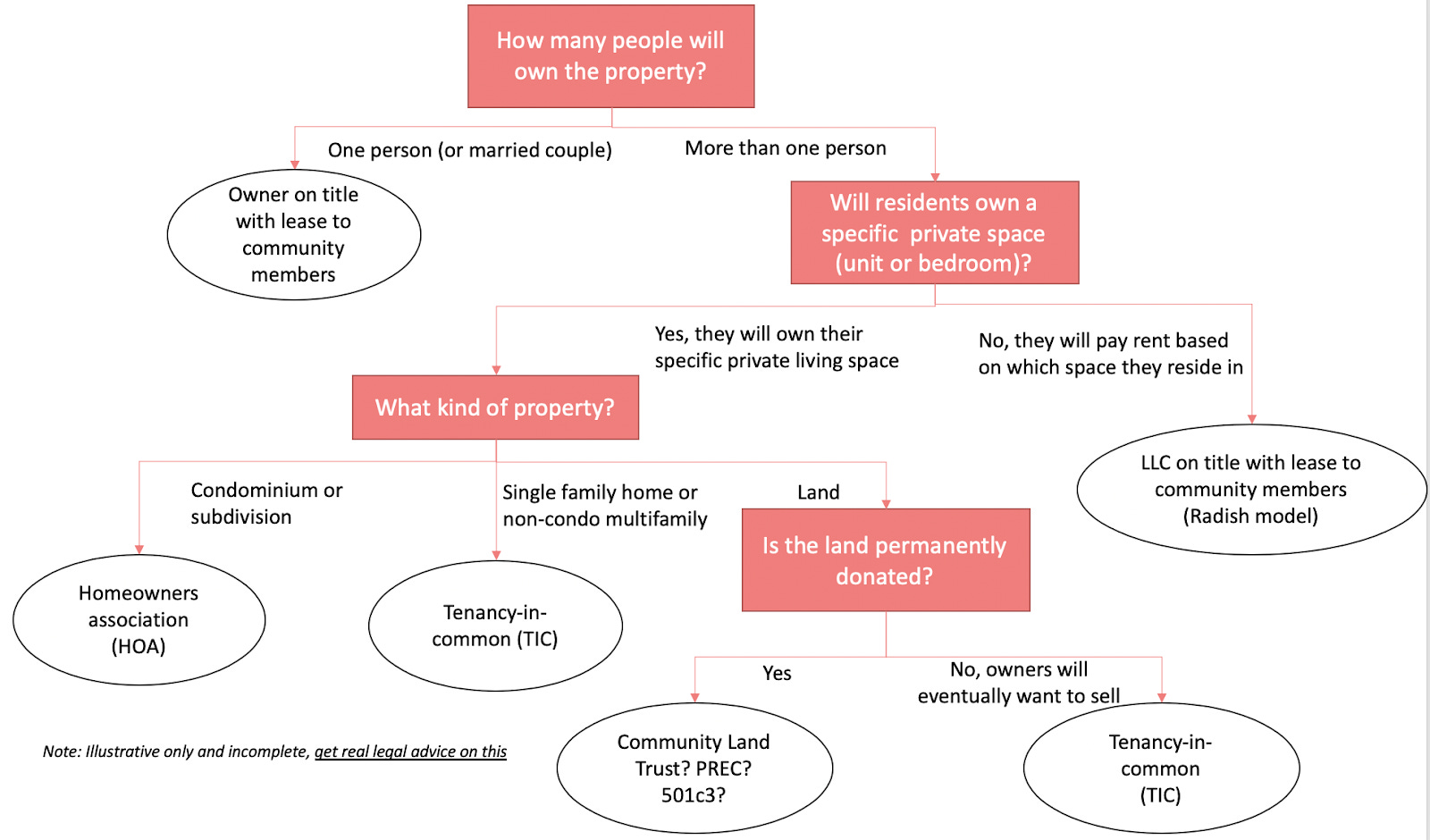

Step 6: Pick a legal structure

The most common question we get at Supernuclear is about legal structures for co-buying. So you might think it’s strange that this hasn’t come up until Step 6. The reason is that the legal structure is an output from the inputs that you decided in the previous steps.

You don’t start with a legal structure. You end with a legal structure.

Here is my best attempt to simplify a complicated problem. This is a good starting point, it’s not the only research you should do on the topic.

Your legal structure is mostly going to depend on two questions: 1) What kind of property is it and 2) Are there renters or just resident-owners who don’t pay rent?

Most people will end up with either an LLC, HOA, TIC, or individual on title. Andy Sirkin’s website is a great resource to learn more about these. There are also some interesting, but less-common alternative structures (PRECs, community land trusts) that optimize for long-term community ownership.

My two cents: If you want to make your life easy, go with a more vanilla business-y structure (e.g. LLC). The banks get it, the insurance company gets it, your investors will get it. A lot less explaining to do and a lot more templates out there for how to do it. If you want to help pioneer new forms of property ownership, by all means do (and please share what you learn!). Experimentation here is commendable. And there are lots of passionate people, seeking a better world, who will help you figure it out. But the trail is less trodden. [note: We’d love to hear from folks using these structures in real projects … hi@gosupernuclear.com].

The Radish LLC Model

[Here’s a more detailed post on the Radish FriendLLC model]

We like the Radish LLC Model and think it has broad applicability to a range of situations. So we are going to dive into how it works.

As the above diagram shows, the Radish Model applies when a) there are multiple owners b) residents pay rent to the owners rather than buy their living space outright. In this model owners and residents wear separate hats. They may overlap, but they conceptually play separate roles.

I am an owner. I am also a resident.

As a resident, I pay rent into the LLC (“Big Cabbage LLC”).

As an owner, I receive cash dividends every quarter from the LLC.

The difference between my dividend and my rent is my “effective rent.”

Some people have a greater ownership stake than their rent (i.e. they own 20% of the property but only pay 10% of the rent on the property due to the size of their living space). They get paid by the system every month.

Some people have a greater rent than their ownership stake. They pay into the system every month.

Everyone can choose where they want to be on this continuum: Own more or rent more … it’s your choice. You can move living spaces and your rent changes. You can sell shares in the LLC and your ownership changes. There’s fluidity and movement.

Owners make owner decisions, such as “when do we sell” (via Kristen and I who are the managers in the LLC).

Residents make resident decisions, such as “who else lives here” and “how we organize a shared food system.”

As an owner and a resident, I participate in decisions at both levels.

And tax time comes, every owner gets a K1 with their profit and loss from the year. From the IRS’s perspective (and the bank, and the insurance company), we are a normal real estate investment LLC. All of the external-facing aspects of this look very conventional to the real estate universe (which we think is good). All of the weird community stuff happens at the community level. The LLC is the nerdy front wearing the suit and tie.

——

Okay, that was a big section….

Here are some common mistakes we see with The How:

Not pausing to face the music on whether you have the right “Who” and “What:” Many groups will not have enough financial resource to get a project done and need to go back and reevaluate these steps. The earlier you can pressure test them, the better.

Being loosey goosey about decision rights: These are BIG decisions impacting hundreds of thousands of people’s dollars. Take them seriously and make everything explicit.

Overcomplicating legal structures: Keep it simple and flexible. Don’t reinvent everything in the universe.

[to my hippies out there] Not wanting to confront the capitalism of the situation: Co-buying property is getting up close and personal with some serious capitalism. Banks, investors, insurance companies. You can play the game however you want, but the parties you need along the way are under no obligation to play along. You’ll need to figure out how to stay true to your values, but also make something happen in a world where property is a highly valued asset.

The Where: Find a property

Now a bit on how to actually find your dream property….

Step 1: Define your archetype

Start with what kind of property you want to buy (your “archetype”). And take note: Not all properties are equal in terms of difficulty.

Single family homes (even huge homes) are easy because our entire homeownership system is built up around them. My advice: If a single family home works for your group, do it!

Vacant apartment buildings with 4 or fewer units are the next easiest. Vacant is key here. Things get much more complicated if there are people living there already. [There’s a lot written about displacement of renters, particularly in the Bay Area, and I’d encourage you to educate yourself on the topic if you are considering buying a tenant-occupied property.]

5+ units is considered a commercial multifamily property by cities and banks. At the level, things get a bit more complicated and often costly.

Purchasing two properties next to each other is another hard-ish option. The hard part is making the offers line up so you don’t get stuck with one property and not the other one. These properties can also be hard to identify because there is no easy way to search for them. But they are a great option if the stars align.

The hardest project of all is developing empty land. It has all the challenges of the above projects plus the difficulty of designing and building. The outcome can be spectacular, but you are in for a slog!

—

Here are a few factors that can add bonus difficulty to an existing archetype:

+10 difficulty points:

Major interior renovations needed

Building an accessory dwelling unit (ADU) [note: We think buying a single family home and building an ADU is a great way to get a lot of living space relatively easily]

+20 difficulty points:

Building a new unit (non-ADU)

Installing major infrastructure - e.g. road, electric or water main

+30 difficulty points:

Changing zoning

Step 2: Begin the on-market search + email alerts

“On-market” refers to public real estate for-sale listings. Depending on property type, you are likely going to use aggregators like Zillow/Redfin/Trulia or commercial aggregators like Loopnet.

Email alerts are your friend. Get a stream of properties into your inbox to get a feel for the market. In hot markets like the Bay Area, property doesn’t stay on the market long. Expect to have less than a couple weeks to make an offer. No email alerts = missing your dream property.

Step 3: Do an off-market search

An off-market search is looking for property that is not formally being sold on the open market. Usually you enlist a real estate agent to help you. They might make cold offers to properties that are not currently listed for sale. They might also know of someone looking to sell soon who hasn’t yet put their property on market. A lot of the best deals happen off-market. But it takes effort to find them.

Common mistakes we see with The Where:

Picking really hard projects to start: e.g. developing an Ecovillage on empty land

Not exploring off-market property: Get an agent to work for you! They get paid regardless when you buy so no extra cost.

Righto!

Now you’ve made an offer. Congrats. Your reward: A whole new set of things to figure out - inspection, closing, permits, renovations.

But we’ll leave that for a future post. Thanks for reading this far. You win a puppy.

Are you going through this process now? We’d love to hear from you and happy to give advice. Hit us up at hi@gosupernuclear.com.

Curious about coliving or co-buying? Find more case studies, how tos, and reflections at Supernuclear: a guide to coliving. Sign up to be notified as future articles are published here:

I come back to this often. One of the most inspiring pieces of writing on the internet imo

This is such a helpful road map. Thank you!